.svg?sfvrsn=be606e78_3)

- Home

- Article

Business Advisor: Which Costing System Is Right for You?

By: Jason Trudell, DBA(c), MHA, MSN, CRNA

Published: 2/1/2024

Share:

Making sense of proposal methods for anesthesia services.

Costing systems are essential to the sustainability and profitability of any successful anesthesia practice.

These systems provide a framework for accurately estimating, allocating and managing labor costs associated with anesthesia, a critical component of every surgery center. Understanding the intricacies of different costing systems and their role in decision analysis support for proposal submission has significant implications for the success or failure of a business venture. Here are two examples.

Time-based costing

Time-based costing is routinely utilized in practices to compensate anesthesia providers systematically. It’s a methodology businesses use to allocate costs based on the time spent on specific activities or tasks. This approach ensures that expenses are distributed proportionately to the time and effort invested. In practice, time-based costing enables the precise determination of payroll costs associated with each anesthesia provider’s activities, such as patient care, teaching, research and administrative duties. Anesthesia providers’ work involves a diverse range of tasks, making it essential to capture the time spent providing services to the organization accurately. This type of costing relies on accurate time-tracking mechanisms, which typically include electronic timesheet systems or application-based software tools that record start and end times for each clinician. By capturing time data, anesthesia practices gain insight into the true effort invested by each provider and can appropriately allocate compensation.

One of the primary advantages of time-based costing for payroll management is the ability to ensure fair compensation for anesthesia providers. Unlike traditional models that may allocate payroll expenses based on fixed salaries or predetermined hourly rates, time-based costing acknowledges the variation in activities and off-shift requirements performed by providers. It enables the differentiation of compensation based on each task’s complexity and time requirements, ensuring that providers are adequately remunerated for their efforts. Time-based costing also facilitates enhanced efficiency within an anesthesia practice by promoting better resource allocation. By capturing detailed time data, leadership can identify areas where clinicians may be spending excessive time or where tasks can be streamlined. This insight allows for more effective planning, scheduling and staffing decisions, all while optimizing resources and reducing waste. Time-based costing also enables administrators to identify potential bottlenecks or areas for improvement in operational processes, leading to greater overall workflow efficiency.

RVU costing

Relative Value Unit (RVU) costing is the standardized methodology for anesthesia billing. It assigns a numerical value to various medical procedures or services based on their complexity, time requirements and resource utilization. Anesthesia services require a comprehensive system for determining appropriate reimbursement. RVU costing offers a standardized and transparent approach to calculating the relative worth of different anesthesia procedures, facilitating accurate billing and reimbursement for the anesthesia provider and the healthcare facility.

In the case of an anesthesia management company, the volume of services provided is a crucial driver. This can be measured by calculating the number of procedures, patient encounters or anesthesia hours. The company collects data on the volume of services for a specific period and current procedural terminology (CPT) code by surgical specialty. There are multiple ways to calculate revenue per RVU of service, as each CPT code is associated with a base RVU unit plus additional time units based on the duration of the surgical procedure. Base RVUs are composed of three components:

- work RVU (wRVU),

- practice RVU (pRVU), and

- malpractice RVU (mRVU).

The wRVU reflects the relative time, skill, effort and expertise involved in performing a particular procedure. The American Medical Association’s Relative Value Scale Update Committee assesses the wRVUs for medical services — including anesthesia procedures — through a rigorous process involving expert input and data analysis. The pRVUs encompass costs associated with operating a practice. RVUs capture the direct and indirect costs of providing medical services, such as equipment, supplies, administrative expenses and nonphysician personnel. These RVUs account for the overhead expenses incurred by anesthesia practices during the delivery of services. The mRVUs account for the cost of provider malpractice insurance and other related liability expenses associated with each procedure.

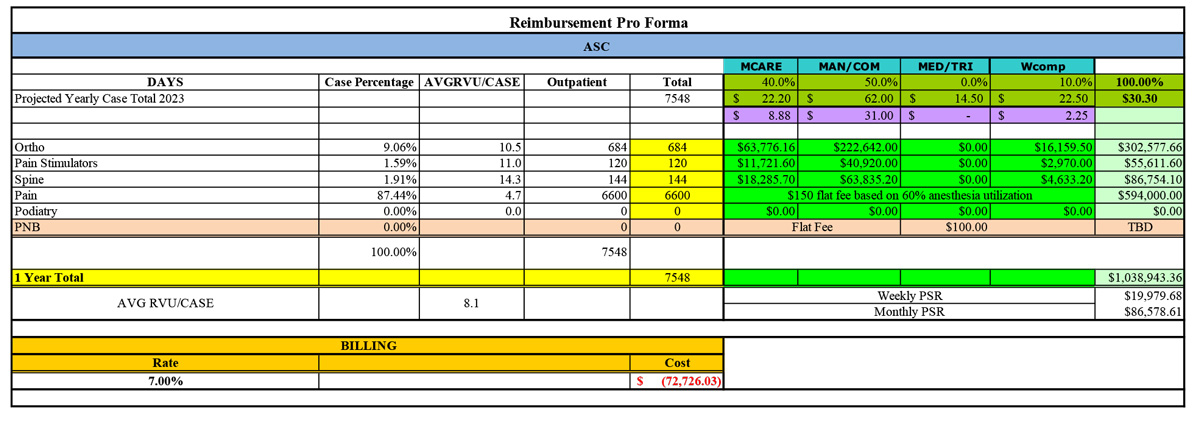

Revenue per RVU of service is typically calculated by categorizing the case volume by payer type. This can vary widely by a practice’s location. Still, the minimum payer categories are Medicare (MCARE), MAN/COM (managed care/commercial), MED/TRI (Medicaid/Tricare) and Workers’ compensation (Wcomp). Internal calculations by subject matter experts in coding then assess the average RVU per case (AVGRVU/CASE) by base CPT and calculate time units. Finally, a mathematical analysis based on total RVUs, weighted payor percentage and derived insurance rate is used to determine the patient service revenue (PSR). Reimbursement exceptions exist based on a service two (TOS2) charge, which excludes time units and is reimbursed at straight CPT rates. Specific surgical procedures are routinely denied anesthesia reimbursement (See chart) by government and commercial payers, and a flat fee structure is proposed to the client in such instances.

Decision-making insight

Anesthesia management companies use various costing tools to assist in planning and decision-making on vendor service proposals, the complexity of which we’ve only scratched the surface of with the above descriptions. Incorporating multiple cost management tools — such as cost-volume processing, job costing and process costing — is very important in calculating accurate financials for new business opportunities. Cost-management tools play a critical role in accurately assessing and presenting the financial aspects of a service proposal. Process costing and average RVU per case are imperative in calculating revenue generation. At most ASCs, the duration of identical surgical procedures can be closely approximated with minimal time variance.

The use of multiple costing tools provides valuable insight for decision-making in anesthesia vendor contracts. By quantifying costs and determining the cost drivers for each process, decision-makers can evaluate the impact of alternative strategies in assessing the feasibility of new initiatives, resource allocation and process improvements, ensuring that the anesthesia service proposal remains financially viable and competitive. OSM

.svg?sfvrsn=56b2f850_5)